Weibold Academy: The global cost of linearity – what the value gap reveals

Weibold Academy article series discusses periodically the practical developments and scientific research findings in the end-of-life tire (ELT) recycling and pyrolysis industry.

These articles are reviews by Claus Lamer – the senior pyrolysis consultant at Weibold. The reviews aim to give industry entrepreneurs, project initiators, investors, and the public a better insight into a rapidly growing circular economy. At the same time, this article series should stimulate discussion.

For completeness, we would like to emphasize that these articles are no legal advice from Weibold or the author. Please refer to the responsible authorities and specialist lawyers for legally binding statements.

Introduction

Circularity has often been discussed in tons: tons collected, tons recycled, tons diverted from landfill, tons of CO₂ avoided. These figures remain important. But they do not fully explain why circularity matters to companies, investors, and policymakers.

The Circularity Gap Report 2026: The Value Gap makes a useful shift. It asks what the cost of linearity is to the economy.

That is a more commercial question. It is also a more uncomfortable one.

According to Circle Economy’s first estimate, the global economy loses around €25.4 trillion per year due to avoidable value loss associated with linear material use. This is equivalent to almost 31% of global Gross Domestic Product (GDP). In simple terms: for every €3 of economic value created, about €1 is lost through waste, inefficiency, premature disposal, energy losses, or asset deterioration.

This should be read carefully. The number is not a direct accounting deduction from GDP. It is an estimate, with methodological limitations. But it is still useful because it makes visible something that industrial companies experience every day: materials are expensive, assets are underused, outputs are undervalued, and waste often contains more value than the market is prepared to recognize. For the tire recycling and pyrolysis sectors, this is highly relevant.

From circularity as compliance to circularity as value retention

For many years, recycling policy has been built around the waste hierarchy: prevent, reuse, recycle, recover, dispose. This remains the right logic. But in practice, industrial markets often treat circularity as a compliance activity rather than a value-retention strategy.

The Value Gap approach helps correct that.

A tire at the end of its life is not only waste. It is a manufactured product containing rubber, carbon black, steel, textile reinforcement, additives, embedded energy, and years of industrial know-how. When it is landfilled, poorly burned, exported through weakly controlled channels, or processed for low-value applications despite higher-value options being available, value is lost.

The same applies to plastics, composites, construction materials, metals, textiles, and machinery. The circular economy is not only about moving material away from disposal. It is about keeping the highest possible level of utility for as long as economically and technically feasible.

This distinction matters. Recycling is sometimes presented as the final solution. In reality, recycling is one tool. Repair, retreading, reuse, remanufacturing, refurbishment, material upgrading, and high-quality secondary raw material production often retain more value than basic material recovery.

For end-of-life tires, this hierarchy is visible in practice. A retreadable tire retains more product value than a tire shredded into chips. A well-specified rubber granulate application usually retains more value than uncontrolled energy recovery. Recovered carbon black and tire pyrolysis oil (TPO) can retain and recreate industrial value, but only if quality, consistency, legal status, and market acceptance are in place.

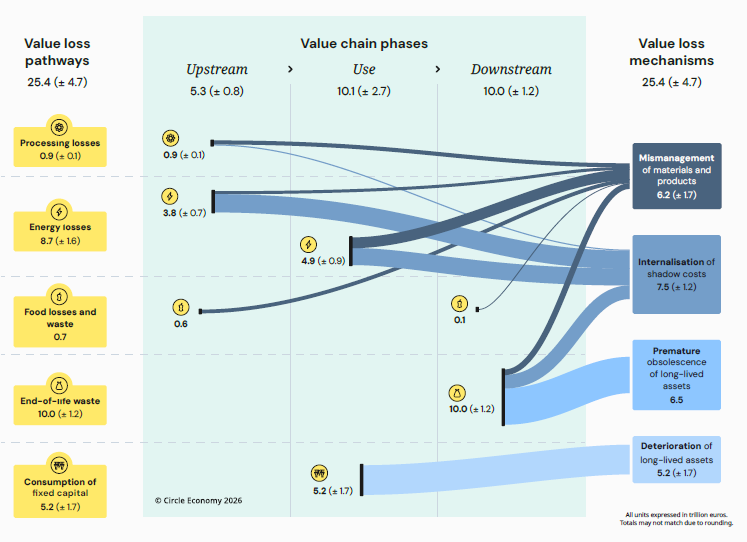

The five loss pathways — and what they mean for recycling

The report groups value loss into five pathways.

The largest is end-of-life waste, estimated at about €10.0 trillion annually. This category is especially important for the recycling industry because it describes the point at which products and assets are discarded while still containing value. Recycling captures part of this value, but usually not all of it. Once a product is dismantled or destroyed, component-level and product-level value are often gone.

Energy losses are estimated at about €8.7 trillion. This is a reminder that circularity and energy efficiency are connected. Pyrolysis operators understand this directly: process gas use, heat integration, oxidizer efficiency, drying, oil upgrading, and carbon handling all affect whether the business case is robust or fragile. A circular process with poor energy management risks losing part of the value it is trying to recover.

Consumption of fixed capital accounts for about €5.2 trillion. This refers to the avoidable deterioration of buildings, infrastructure, machinery, and other long-lived assets. For recyclers, this is not abstract. Plant reliability, maintenance strategy, equipment lifetime, modular design, and upgradeability are all circularity issues. A plant that is poorly maintained or prematurely obsolete destroys capital value and weakens investor confidence.

Processing losses are estimated at about €904 billion. These are losses during the transformation of raw materials into intermediate or final products. In recycling, processing losses are familiar: fines, off-spec fractions, contamination, unrecovered metals, inconsistent char quality, volatile yields, rejected batches, and residues requiring costly treatment. Better sorting, pre-treatment, process control, and quality assurance are therefore not only operational improvements. They are value-retention measures.

Food losses and waste, estimated at about €651 billion, may appear less relevant to tire recycling. But the underlying lesson is the same: supply chain coordination, logistics, storage, quality control, and demand matching often determine whether value is preserved or lost.

Why GDP misses the problem

One of the Circularity Gap Report’s strongest arguments is that conventional economic indicators measure activity rather than value retention.

Gross Domestic Product (GDP) records production and transactions. It does not adequately show whether natural capital is depleted, whether products are discarded too early, whether assets are underutilized, or whether pollution costs are pushed onto society. Cleaning up damage can even increase measured economic activity, while the original loss remains poorly visible.

This is a familiar problem in recycling markets. Virgin materials can appear cheaper because environmental costs, depletion risks, and future waste-management burdens are not fully priced. Secondary materials can appear expensive because they must bear the real costs of collection, sorting, processing, certification, and compliance from day one.

That is not a level playing field.

If circular materials are expected to compete only on short-term prices with virgin materials that do not internalize their full costs, many circular business cases will remain difficult to pursue. This is particularly true for recovered carbon black, advanced rubber powders, pyrolysis oil, and other outputs requiring technical upgrading and customer qualification.

What the report means for tire recycling and pyrolysis

The report strengthens the strategic case for tire recycling in four ways.

First, it supports a broader definition of value. ELTs should not be assessed only by disposal cost or gate fee. Their value depends on what can be retained: rubber functionality, carbon content, steel value, oil fractions, energy content, avoided emissions, and reduced dependence on virgin resources.

Second, it highlights the importance of product quality. Low-quality outputs may move material out of the waste stream, but still lose substantial value. High-quality circular products require investment in process control, testing, standards, and customer development.

Third, it makes the financial argument clearer. Investors are more likely to support circular projects when value retention can be quantified. This includes avoided waste cost, recovered material revenue, supply resilience, lower exposure to virgin input volatility, and regulatory alignment.

Fourth, it reinforces the need for better policy. Markets cannot close the Value Gap alone if regulation remains fragmented. End-of-waste rules, product status, REACH and CLP interfaces, mass-balance recognition, public procurement, recycled-content demand, and cross-border movement of waste all influence whether circular value is captured or lost.

Value loss pathways and drivers across the value chain

Source: Circle Economy. (2026). The Circularity Gap Report 2026: The Value Gap. Amsterdam: Circle Economy (pg. 25).

A useful number, but not a final number

The €25.4 trillion estimate should not be treated as a precise invoice. Circle Economy is transparent that this is a first attempt and that the methodology will need refinement. Some externalities are only partially included. Service-sector value losses are not fully captured. Transition costs are not deducted. Results should be interpreted as indicative potential, not guaranteed savings.

That does not weaken the Circularity Gap Report. It makes it more credible.

Circularity has suffered in the past from inflated claims and vague slogans. The stronger approach is to acknowledge uncertainty while improving the evidence base. The Value Gap is useful because it gives companies and policymakers a starting point for asking better questions.

Where is value lost? Who bears the cost? Which losses are technically avoidable? Which require new infrastructure? Which require regulation? Which can be solved by business model innovation? Which depend on demand-side measures?

These are the right questions for the next phase of circular economy policy.

Conclusion

The Circularity Gap Report 2026 gives the circular economy a sharper economic language. It shows that linearity is environmentally damaging. It is economically wasteful.

For the recycling industry, this is an important shift. It moves the discussion from waste handling to value retention. It also makes clear that the next stage of circularity will be judged not only by how much material is recycled, but by how much value is preserved.

For tire recycling and pyrolysis, the implication is clear: the sector should position itself not as a disposal outlet but as part of the industrial value-retention infrastructure that Europe and all the other regions increasingly need.

That requires better plants, better data, better output quality, better standards, and better regulation. It also requires a more honest discussion in the market. If circular materials are expected to compete in markets where linear losses remain invisible, the Value Gap will not close.

The report’s central message is therefore simple: circularity is not a cost to be tolerated. Properly designed, it is a way to stop losing value.

Copyright: ©2026 by Robert Weibold GmbH. This article is an open-access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license CC BY 4.0. You must give appropriate credit, provide a link to the license and this article, and indicate if changes were made. You may do so in any reasonable manner, but not in any way that suggests the licensor endorses you or your use.

Weibold is an international consulting company specializing exclusively in end-of-life tire recycling and pyrolysis. Since 1999, we have helped companies grow and build profitable businesses.